Key points

- Tractor Supply Company had a solid quarter, but results were as expected and forecasts were lukewarm.

- Cash flow and capital returns remain robust and will continue to pay shareholders and reduce share counts in 2024.

- Analysts support the stock but may not provide a catalyst until later in the year.

- 5 stocks we like best from Tractor Supply

Tractor supply company NASDAQ:TSCO it can reach new heights in 2024, but it could be a tough slog for stock prices and shareholders. While the fundamental framework is solid and the outlook for capital returns robust, the headline findings could weigh on price action. The company posted a tepid outlook for the year, forecasting only mild revenue growth and a stable margin, which in most cases is not a catalyst for a rally.

Margin, cash flow, balance sheet and capital returns will drive this market.

Tractor Supply Company reaps quality profits

Tractor Supply Company has enjoyed the dual benefit of pandemic-related spending and a CEO-led turnaround for years. Now, as COVID-affected spending habits normalize or normalize, the story hinges on the efforts of CEO Hal Lawton, who continues to pay forward these retail stocks. Fourth quarter results reflect the impact of declining demand and the company’s strengths, including cost-effective operations, consumer loyalty and margin quality.

Tractor Supply Company reported revenue of $3.66 billion, down 8.7% from last year and as expected. However, the decline is partly due to one less week in the operating period, worth 560 basis points, and the comparison with last year is difficult.

Fourth-quarter revenue in F2022 was a record $4.01 billion, up 20% from the previous year’s record, leaving this year’s result the second-highest quarter on record. In this light, a small return is nothing that investors need to worry about. Comps are down, but traffic remains solid with an increasing number of stores to provide leverage. The company added 22 net new stores in the fourth quarter for a year-over-year (YOY) gain of 0.8%, and expansion is expected to continue into 2024.

The news on margins is good. The company reduced gross margin and selling, general and administrative expenses compared to last year, bolstering profits. Gross margin improved 130 basis points and SG&A fell 400 basis points, but increased as a percentage of revenue to leave GAAP earnings at $2.28 – six cents, or 260 basis points, better than the consensus estimate of MarketBeat.com, and play into capital return prospects.

Forecasts for next year are slightly below consensus, but call for modest revenue growth and stable earnings, sufficient to support robust capital return prospects.

Tractor Supply Company creates shareholder value

Tractor Supply Company is creating value by growing the business and repurchasing stock. Repurchases in F2023 were sufficient to reduce the diluted share count by 2.2% year-over-year, including stock-based compensation and stock sales. Fourth-quarter buybacks more than doubled the dividend yield, which was solid at 1.8%. Forecasts for the year include an expectation of stable buybacks in 2024 versus 2023, with a dividend increase compounding the picture.

Tractor Supply is a solid growth stock in distribution, on track to achieve Dividend Aristocrat status. The company has been growing for 14 consecutive years and pays out less than 40% of its earnings, with long-term growth expected. The balance sheet features low debt, growing liquidity and growing equity capital. Shares are up 5% year-over-year after rising 20% in F2022.

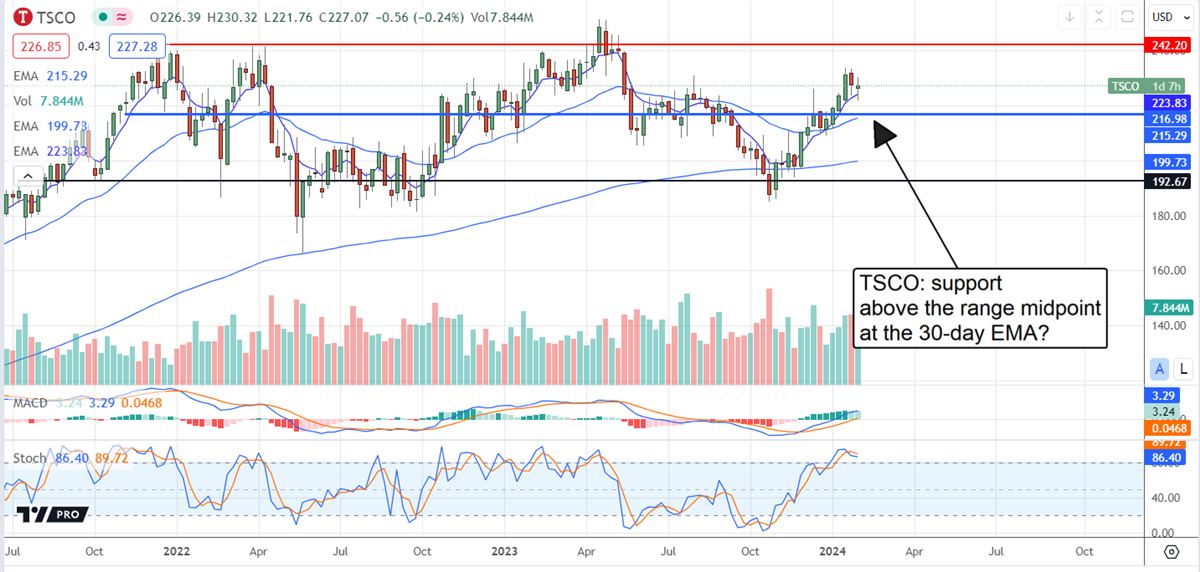

The technical outlook: Tractor Supply Company is limited

The Tractor Supply Company has been stuck for three years and is unlikely to emerge now. The post-release action has led the market to move lower and may soon retest support in the middle part of the range. This is the critical target and short sellers are in the mix. Short interest was above 10% in the last report and may not fall much now.

A move below the average range could send the stock to the low range near $190, but if support is confirmed, a move towards the high range should be expected. Among the potential catalysts for a new high is the dividend. The next distribution increase is expected soon and could be large. The company has a CAGR of 30%, but recent increases have been closer to 10%, which is likely now.

Before you consider Tractor Supply, you’ll want to hear this.

MarketBeat tracks Wall Street’s highest-rated and best-performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market takes hold… and Tractor Supply wasn’t on the list.

While Tractor Supply currently has a “Hold” rating among analysts, top analysts believe these five stocks are better buys.

View the five stocks here

What stocks are being purchased by major institutional investors, including hedge funds and endowments, in today’s market? Click the link below and we’ll send you MarketBeat’s list of thirteen stocks that institutional investors are buying as fast as they can.

Get this free report